|

Arrangement of Sections

|

-

LEGAL TENDER OF EAST AFRICAN SHILLINGS

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF BANKNOTES

-

LEGAL TENDER OF EAST AFRICAN SHILLINGS

-

THE CENTRAL BANK OF KENYA- DETERMINATION OF PAR VALUE OF THE KENYA SHILLING

-

THE CENTRAL BANK OF KENYA- DETERMINATION OF PAR VALUE OF THE KENYA SHILLING

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW NOTES, 1970

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF BANK NOTES, 1970

-

LNSTRUCTIONS TO SPECIFIED FINANCIAL LNSTITUTIONS

-

LNSTRUCTIONS TO SPECIFIED FINANCIAL LNSTITUTIONS

-

LNSTRUCTIONS TO SPECIFIED FINANCIAL LNSTITUTIONS

-

THE CENTRAL BANK OF KENYA ACT- DETERMINATION AS TO THE PAR VALUE OF THE KENYA SHILLING, 1971

-

THE CENTRAL BANK OF KENYA ACT- DETERMINATION AS TO THE PAR VALUE OF THE KENYA SHILLING

-

THE CENTRAL BANK OF KENYA ACT- WITHDRAWAL OF EAST AFRICAN SHILLINGS, 1972

-

THE CENTRAL BANK OF KENYA ACT- WITHDRAWAL OF EAST AFRICAN SHILLINGS, 1972

-

THE CENTRAL BANK OF KENYA ACT- DETERMINATION OF PAR VALUE OF THE KENYAN SHILLING, 1973

-

THE CENTRAL BANK OF KENYA ACT- DETERMINATION OF PAR VALUE OF THE KENYAN SHILLING, 1973

-

DETERMINATION OF PAR VALUE OF THE KENYAN SHILLING, 1973

-

CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW COIN, 1973

-

CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW COIN, 1973

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF BANK NOTES, 1974

-

THE CENTRAL BANK OF KENYA ACT- WITHDRAWAL OF BANK NOTES, 1974

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF BANK NOTES, 1974

-

THE CENTRAL BANK OF KENYA ACT- WITHDRAWAL OF BANK NOTES, 1974

-

SPECIFIED PUBLIC ENTITIES UNDER SECTION 2

-

SPECIFIED PUBLIC ENTITIES UNDER SECTION 2

-

SPECIFIED PUBLIC ENTITIES UNDER SECTION 2

-

SPECIFIED PUBLIC ENTITIES UNDER SECTION 2

-

SPECIFIED PUBLIC ENTITIES UNDER SECTION 2

-

SPECIFIED PUBLIC ENTITIES UNDER SECTION 2

-

THE CENTRAL BANK OF KENYA- DESCRIPTION OF BANK NOTES, 1979

-

THE CENTRAL BANK OF KENYA- DESCRIPTION OF NEW ISSUE OF COMMEMORATIVE GOLD AND SILVER COINS, 1979

-

THE CENTRAL BANK OF KENYA- DESCRIPTION OF BANK NOTES, 1979

-

THE CENTRAL BANK OF KENYA- DESCRIPTION OF NEW ISSUE OF COMMEMORATIVE GOLD AND SILVER COINS, 1979

-

THE CENTRAL BANK OF KENYA- DESCRIPTION OF NEW KENYA CURRENCY NOTES AND COINS, 1980

-

THE CENTRAL BANK OF KENYA- DESCRIPTION OF NEW KENYA CURRENCY NOTES AND COINS, 1980

-

THE CENTRAL BANK OF KENYA SPECIFIED BANKS AND FINANCIAL INSTITUTIONS, 1983

-

THE CENTRAL BANK OF KENYA SPECIFIED BANKS AND FINANCIAL INSTITUTIONS, 1983

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF SHILLINGS COIN, 1985

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF SHILLINGS COIN, 1985

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF TWO HUNDRED SHILLINGS NOTE, 1986

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF TWO HUNDRED SHILLINGS NOTE, 1986

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF THE CENTRAL BANK OF KENYA'S 20TH ANNIVERSARY COMMEMORATIVE COINS, 1986

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF THE CENTRAL BANK OF KENYA'S 20TH ANNIVERSARY COMMEMORATIVE COINS, 1986

-

WAIVER

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF TEN AND ONE HUNDRED SHILLINGS NOTE, 1989

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF TEN AND ONE HUNDRED SHILLINGS NOTE, 1989

-

THE CENTRAL BANK OF KENYA ACT- INCREASE IN CAPITAL, 1989

-

THE CENTRAL BANK OF KENYA ACT- INCREASE IN CAPITAL, 1989

-

REGULATION OF INTEREST RATES AND TERMS OF CREDIT OF SPECIFIED BANKS AND SPECIFIED FINANCIAL INSTITUTIONS

-

REGULATION OF INTEREST RATES AND TERMS OF CREDIT OF SPECIFIED BANKS AND SPECIFIED FINANCIAL INSTITUTIONS

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF FIFTY SHILLINGS NOTE, 1990

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF FIFTY SHILLINGS NOTE, 1990

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF THE CENTRAL BANK OF KENYA'S SILVER JUBILEE COMMEMORATIVE COINS, 1991

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF THE CENTRAL BANK OF KENYA'S SILVER JUBILEE COMMEMORATIVE COINS, 1991

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW TWENTY SHILLINGS NOTE, 1994

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW TWENTY SHILLINGS NOTE, 1994

-

THE CENTRAL BANK OF KENYA ACT- DETERMINATION, 1994

-

THE CENTRAL BANK OF KENYA ACT- DETERMINATION, 1994

-

THE CENTRAL BANK OF KENYA- DESCRIPTION OF NEW ISSUE OF TEN SHILLINGS (BI-METAL) COIN, 1994

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ONE THOUSAND SHILLINGS NOTE, 1995

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ONE THOUSAND SHILLINGS NOTE, 1995

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF FIFTY CENTS, ONE SHILLING AND FIVE SHILLINGS COINS, 1995

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF FIFTY CENTS, ONE SHILLING AND FIVE SHILLINGS COINS, 1995

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF FIVE HUNDRED SHILLINGS NOTE, 1995

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF TWENTY SHILLINGS NOTE, 1995

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF FIVE HUNDRED SHILLINGS NOTE, 1995

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF TWENTY SHILLINGS NOTE, 1995

-

THE CENTRAL BANK OF KENYA (FOREIGN EXCHANGE BUSINESS) REGULATIONS, 1996

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF FIFTY SHILLINGS NOTE, 1996

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF TEN CENTS COIN, 1996

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF FIFTY SHILLINGS NOTE, 1996

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF TEN CENTS COIN, 1996

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF ONE HUNDRED AND TWO HUNDRED SHILLINGS NOTES, 1996

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF ONE HUNDRED AND TWO HUNDRED SHILLINGS NOTES, 1996

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF FIVE HUNDRED AND ONE THOUSAND SHILLINGS NOTES, 1998

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF FIVE HUNDRED AND ONE THOUSAND SHILLINGS NOTES, 1998

-

THE CENTRAL BANK OF KENYA (DECLARATION OF CURRENCY) REGULATIONS, 1998

-

THE CENTRAL BANK OF KENYA (DECLARATION OF CURRENCY) REGULATIONS

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF TWENTY SHILLINGS COIN, 1999

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF TWENTY SHILLINGS COIN, 1999

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF FIFTY, FIVE HUNDRED AND ONE THOUSAND SHILLINGS CURRENCY NOTES, 2003

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF FIFTY, FIVE HUNDRED AND ONE THOUSAND SHILLINGS CURRENCY NOTES, 2003

-

THE CENTRAL BANK OF KENYA ACT- DECLARATION OF A PUBLIC ENTITY, 2003

-

SPECIFIED BANKS AND FINANCIAL INSTITUTIONS

-

SPECIFIED BANKS AND FINANCIAL INSTITUTIONS

-

SPECIFIED BANKS AND FINANCIAL INSTITUTIONS

-

SPECIFIED BANKS AND FINANCIAL INSTITUTIONS

-

THE CENTRAL BANK OF KENYA ACT- DECLARATION OF A PUBLIC ENTITY, 2003

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF COMMEMORATIVE GOLD AND SILVER COINS, 2003

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF FORTY SHILLINGS COIN AND TWO HUNDRED SHILLINGS NOTE, 2003

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF COMMEMORATIVE GOLD AND SILVER COINS, 2003

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF FORTY SHILLINGS COIN AND TWO HUNDRED SHILLINGS NOTE, 2003

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF FIFTY, ONE HUNDRED, TWO HUNDRED, FIVE HUNDRED AND ONE THOUSAND SHILLINGS CURRENCY NOTES

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF FIFTY, ONE HUNDRED, TWO HUNDRED, FIVE HUNDRED AND ONE THOUSAND SHILLINGS CURRENCY NOTES

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF FIVE CENTS, TEN CENTS, FIFTY CENTS, ONE SHILLING, FIVE SHILLINGS, TEN SHILLINGS AND TWENTY SHILLINGS COINS, 2005

-

THE CENTRAL BANK OF KENYA ACT- DESCRIPTION OF NEW ISSUE OF FIVE CENTS, TEN CENTS, FIFTY CENTS, ONE SHILLING, FIVE SHILLINGS, TEN SHILLINGS AND TWENTY SHILLINGS COINS, 2005

-

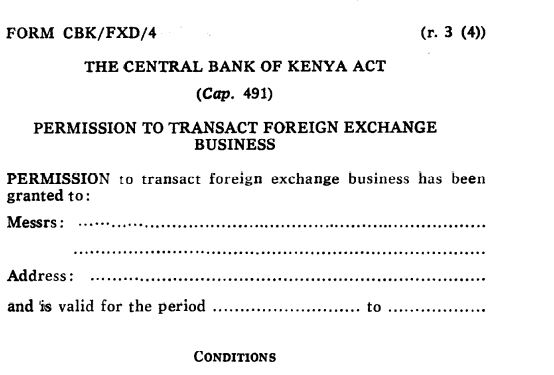

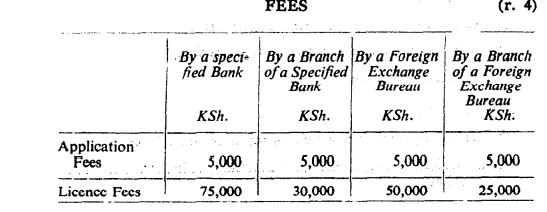

THE CENTRAL BANK OF KENYA (FOREIGN EXCHANGE BUSINESS) REGULATIONS, 2007

-

THE CENTRAL BANK OF KENYA (FOREIGN EXCHANGE BUSINESS) REGULATIONS, 2007

-

THE CENTRAL BANK OF KENYA ACT- SPECIFIED BANKS AND FINANCIAL INSTITUTIONS, 2007

-

THE CENTRAL BANK OF KENYA (CURRENCY HANDLING) REGULATIONS, 2008

-

THE CENTRAL BANK OF KENYA (FOREIGN EXCHANGE BUREAU) (PENALTIES) REGULATIONS, 2009

-

THE CENTRAL BANK OF KENYA (FOREIGN EXCHANGE BUREAU) (PENALTIES) REGULATIONS

-

THE CENTRAL BANK OF KENYA ACT- SPECIFICATION OF BANK, 2009

-

THE CENTRAL BANK OF KENYA (CURRENCY HANDLING) REGULATIONS, 2010

-

THE CENTRAL BANK OF KENYA (CURRENCY HANDLING) REGULATIONS

-

THE CENTRAL BANK OF KENYA (CURRENCY HANDLING) REGULATIONS

-

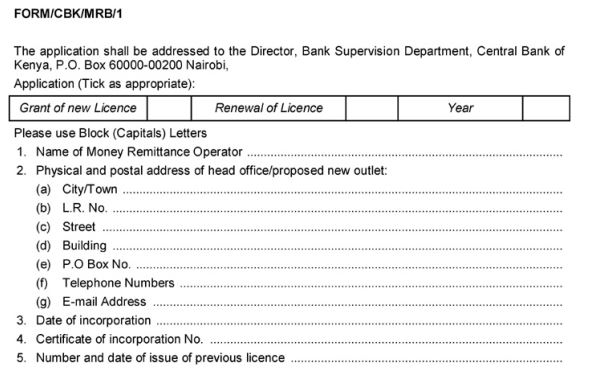

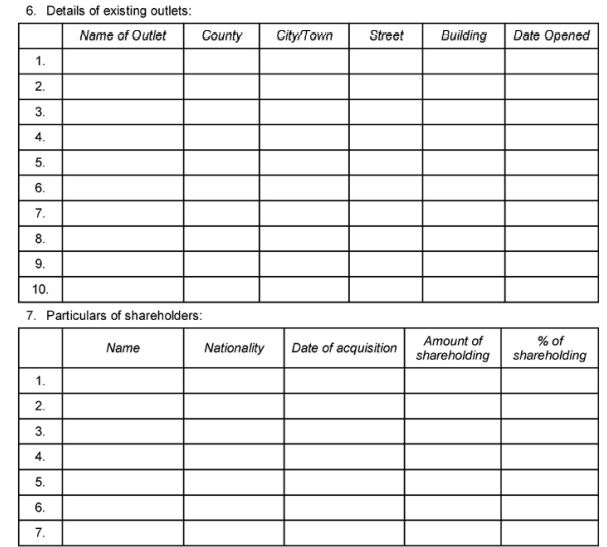

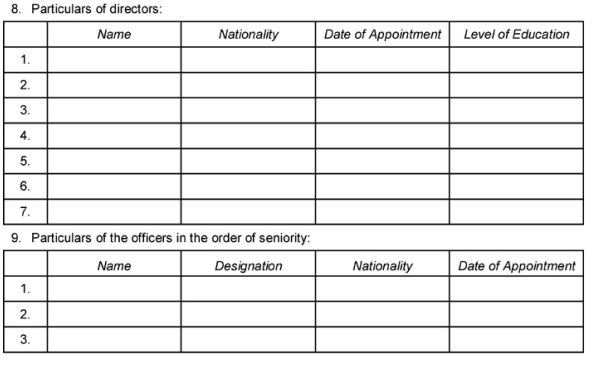

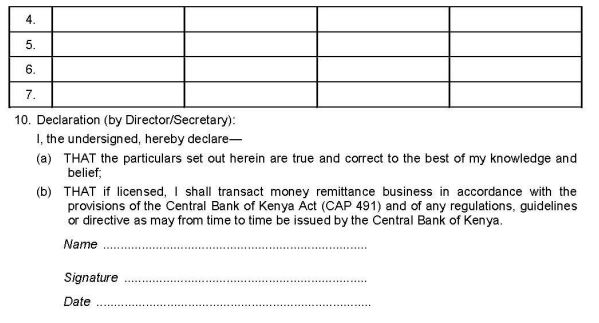

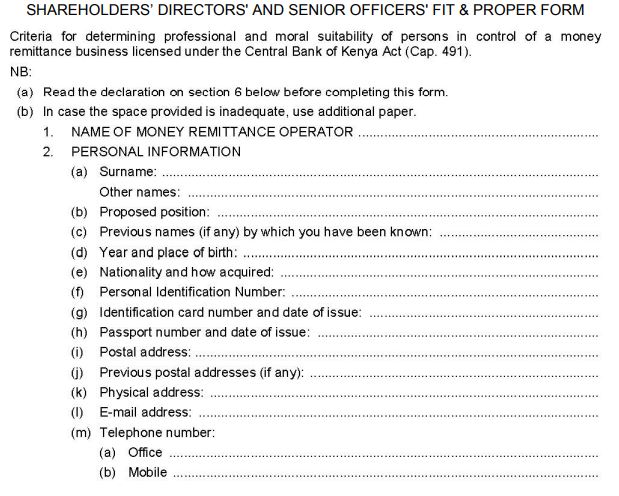

THE MONEY REMITTANCE REGULATIONS, 2013

-

THE MONEY REMITTANCE REGULATIONS

-

THE CENTRAL BANK OF KENYA ACT- SPECIFICATION OF PUBLIC ENTITY, 2013

-

THE CENTRAL BANK OF KENYA ACT- SPECIFICATION OF PUBLIC ENTITY

-

SPECIFICATION OF INSTITUTION

-

SPECIFICATION OF INSTITUTION

-

DESCRIPTION OF NEW ISSUE OF ONE SHILLING, FIVE SHILLINGS, TEN SHILLINGS AND TWENTY SHILLINGS COINS

-

DESCRIPTION OF NEW ISSUE OF ONE SHILLING, FIVE SHILLINGS, TEN SHILLINGS AND TWENTY SHILLINGS COINS

-

DESCRIPTION OF NEW ISSUE OF FIFTY, ONE HUNDRED, TWO HUNDRED, FIVE HUNDRED AND ONE THOUSAND SHILLINGS KENYA CURRENCY NOTES

-

DESCRIPTION OF NEW ISSUE OF FIFTY, ONE HUNDRED, TWO HUNDRED, FIVE HUNDRED AND ONE THOUSAND SHILLINGS KENYA CURRENCY NOTES

-

THE CENTRAL BANK OF KENYA (MORTGAGE REFINANCE COMPANIES) REGULATIONS, 2019

-

THE CENTRAL BANK OF KENYA (MORTGAGE REFINANCE COMPANIES) REGULATIONS, 2019

-

THE CENTRAL BANK OF KENYA (MORTGAGE REFINANCE COMPANIES) REGULATIONS, 2019

|

|

LEGAL TENDER OF EAST AFRICAN SHILLINGS

IN EXERCISE of the powers conferred by section 22 (4) of the Central Bank of Kenya Act 1966, the Minister for Finance, on the recommendation of the Central Bank of Kenya, hereby determines that notes issued by the East African Currency Board shall, in addition to notes issued by the Central Bank of Kenya, remain legal tender in Kenya for one year commencing from the start of the exchange of the notes issued by the East African Currency Board into Kenya currency.

LEGAL TENDER OF EAST AFRICAN SHILLINGS

Revoked by Legal Notice 233 of 1972 on 17th November, 1972

THE CENTRAL BANK OF KENYA- DESCRIPTION OF BANKNOTES

Revoked by Legal Notice 307 of 1974 on 13th December, 1974

IN EXERCISE of powers conferred by section 22 (2) of the Central Bank of Kenya Act 1966, the Minister for Finance acting on the recommendation of the Central Bank of Kenya, hereby determines that the denominations, inscriptions, form and material and characteristics of notes to be issued by the Central Bank of Kenya shall be as follows:—

The notes of the Central Bank of Kenya shall have the denominations of five shillings, ten shillings, twenty shillings, fifty shillings and one hundred shillings and shall be signed for the Board of Directors of the Central Bank of Kenya by the Governor and a member of the Board. The first issue of the aforesaid notes shall be known as that of 1st July 1966.

The designs of the new notes shall show features indigenous to Kenya and in addition to its individual characteristics, described below, each note shall incorporate on the front of the note—

| (a) |

the portrait of the President, His Excellency Mzee Jomo Kenyatta;

|

| (b) |

the title of the Bank in Swahili and English; and

|

| (c) |

an ornamental motif in the centre, incorporating some features of Kenya's coat-of-arms. A lion's head shall be used as the watermark and the paper shall include a security thread.

|

| Sh. |

5

Size: 5 3/4 inches by 3 1/4 inches.

Basic Colour: Green.

Back: Tea pluckers and a tea estate with Mt. Kenya in the background.

|

| Sh. |

20

Size: 6 inches by 34 inches.

Basic Colour: Blue.

Back: Sisal plantation with Mt. Kenya in the background.

|

| Sh. |

50

Size: 6 inches by 3 3/4 inches.

Basic Colour: Grey-brown.

Back: Cotton pickers on a cotton plantation with Mt. Kenya in the background.

|

| Sh. |

100

Size: 6 1/4 inches by 3 3/4 inches.

Basic Colour: Purple.

Back: Cultivators in a pineapple plantation with Mt. Kenya in the background.

|

THE CENTRAL BANK OF KENYA- DESCRIPTION OF BANKNOTES

Revoked by Legal Notice 307 of 1974 on 13th December, 1974

THE CENTRAL BANK OF KENYA- DETERMINATION OF PAR VALUE OF THE KENYA SHILLING

IN EXERCISE of the powers conferred by section 20 of the Central Bank of Kenya Act 1966, the President, acting on the advice of the Central Bank of Kenya, hereby with effect from the 14th September 1966, determines the par value of the Kenya shilling in terms of gold as follows :—

250 Kenya shillings to equal one troy ounce of fine gold.

THE CENTRAL BANK OF KENYA- DESCRIPTION OF NEW NOTES, 1970

Revoked by Legal Notice 307 of 1974 on 13th December, 1974

IN EXERCISE of the powers conferred by subsection (2) of section 22 of the Central Bank of Kenya Act, the Minister for Finance acting on the recommendation of the Central Bank of Kenya hereby determines that in addition to the description of banknotes specified under Legal Notice No. 252 of 1966, the Central Bank of Kenya may issue banknotes of all denominations incorporating the inscription "First President of Kenya Mzee Jomo Kenyatta".

THE CENTRAL BANK OF KENYA- DESCRIPTION OF NEW NOTES, 1970

Revoked by Legal Notice 307 of 1974 on 13th December, 1974

THE CENTRAL BANK OF KENYA- DESCRIPTION OF NEW ISSUE OF BANK NOTES, 1970

Revoked by Legal Notice 307 of 1974 on 13th December, 1974

IN EXERCISE of the powers conferred by section 22 (2) of the Central Bank of Kenya Act, 1966, the Minister for Finance acting on the recommendation of the Central Bank of Kenya, hereby determines that the denominations, inscriptions, form, material and characteristics of new notes to be issued by the Central Bank of Kenya shall be as follows:—

| 1. |

The new notes shall have the denominations of five shillings, ten shillings, twenty shillings, fifty shillings and one hundred shillings.

|

| 2. |

The designs of the new notes shall show features indigenous to Kenya and in addition to its individual characteristics, described below, each note shall incorporate—

| (a) |

on the front of the note—

| (i) |

the portrait of the President, His Excellency Mzee Jomo Kenyatta; |

| (ii) |

an inscription "First President of Kenya Mzee Jomo Kenyatta"; |

| (iii) |

the title of the Bank in Swahili and English followed by words in English "LEGAL TENDER FOR..." and the denomination of the note in words in Swahili; |

| (iv) |

an ornamental motif in the centre, incorporating some features of Kenya's coat-of-arms and depicting the denomination of the note in words in English followed by the words "FOR THE BOARD OF DIRECTORS" underneath which the signatures of the Governor and a member of the Board of Directors of the Bank shall be inscribed. A lion's head shall be used as the watermark and the paper comprising each note shall include a security thread; |

| (v) |

a serial number at the top right hand vicinity of the corner and at the bottom left hand vicinity of the corner; |

| (vi) |

the date of issue of the notes at the bottom right hand vicinity of the corner; |

| (vii) |

the denomination of the note in English figures at the corners of each note. |

|

| (b) |

on the back of the note, in addition to the individual characteristics pertaining to the back, the denominations of the note in English figures at the corners of each note.

|

|

| 3. |

The individual characteristics of the various denomination of notes shall be as follows

|

| Sh. |

5

Size: 5 1/4 inches by 2 3/4 inches.

Basic Colour: Brown.

Back: A coffee picker and coffee plantation with Mt. Kenya in the background.

|

| Sh |

10

Size: 5 3/4 inches by 3 1/4 inches.

Basic Colour: Green.

Back: Tea pluckers and a tea estate with Mt. Kenya in the background.

|

| Sh. |

20

Size: 6 inches by 3 1/2 inches.

Basic Colour: Blue.

Back: Sisal plantation with Mt. Kenya in the background.

|

| Sh. |

50

Size: 6 inches by 3 3/4 inches.

Basic Colour: Grey-brown.

Back: Cotton pickers on a cotton plantation with Mt. Kenya in the background.

|

| Sh. |

100

Size: 6 ¼ inches by 3 3/4 inches.

Basic Colour: Purple.

Back: Cultivators in a pineapple plantation with Mt. Kenya in the background.

|

THE CENTRAL BANK OF KENYA- DESCRIPTION OF NEW ISSUE OF BANK NOTES, 1970

Revoked by Legal Notice 307 of 1974 on 13th December, 1974

LNSTRUCTIONS TO SPECIFIED FINANCIAL LNSTITUTIONS

| (1) |

With effect from the 27th day of July, 1971, the minimum cash deposit in respect of hire-purchase agreements relating to the purchase of new private motor-cars, imported furniture, carpets and electrical household equipment shall be 40 per cent of the cash price as required under section 6(1) of the Hire-Purchase Act, 1968 (No. 42 of 1968).

|

| (2) |

The volume of credit granted in respect of hire-purchase agreements with hirers shall not exceed the total amount of out-standings as at the 26th day of July, 1971.

|

| (3) |

The volume of credit by way of advance or loan against, or discount of hire-purchase agreements granted to persons licensed to carry on hire-purchase business under Part VII of the Hire-Purchase Act, 1968, shall not exceed the total amount of outstandings as at the 26th day of July, 1971.

|

LNSTRUCTIONS TO SPECIFIED FINANCIAL LNSTITUTIONS

| (1) |

With effect from the 27th day of July, 1971, the minimum cash deposit in respect of hire-purchase agreements relating to the purchase of new private motor-cars, imported furniture, carpets and electrical household equipment shall be 40 per cent of the cash price as required under section 6(1) of the Hire-Purchase Act, 1968 (No. 42 of 1968).

|

| (2) |

Deleted by L.N. 50 of 1973.

|

| (3) |

Deleted by L.N. 50 of 1973.

|

LNSTRUCTIONS TO SPECIFIED FINANCIAL LNSTITUTIONS

| (1) |

With effect from the 27th day of July, 1971, the minimum cash deposit in respect of hire-purchase agreements relating to the purchase of new private motor-cars, imported furniture, carpets and electrical household equipment shall be 40 per cent of the cash price as required under section 6(1) of the Hire-Purchase Act (Cap. 507).

|

| (2) |

Deleted by L.N. 50 of 1973.

|

| (3) |

Deleted by L.N. 50 of 1973.

|

THE CENTRAL BANK OF KENYA- DETERMINATION AS TO THE PAR VALUE OF THE KENYA SHILLING, 1971

IN EXERCISE of the powers conferred by section 20 of the Central Bank of Kenya Act, I, Jomo Kenyatta President and Commander-in-Chief of the Armed Forces of the Republic of Kenya, acting on the advice of the Central Bank of Kenya, hereby with effect from the 23rd December, 1971, determine the par value of the Kenya Shilling in terms of gold as follows:—

271.42857 Kenya Shillings to equal one troy ounce of fine gold.

THE CENTRAL BANK OF KENYA- DETERMINATION AS TO THE PAR VALUE OF THE KENYA SHILLING

With effect from 23rd December, 1971, the par value of the Kenya Shilling in terms of gold as 271.42857 Kenya Shillings to equal one troy ounce of fine gold.

THE CENTRAL BANK OF KENYA- WITHDRAWAL OF EAST AFRICAN SHILLINGS, 1972

IN EXERCISE of the powers conferred by section 23 of the Central Bank of Kenya Act, the Central Bank of Kenya, with the approval of the Minister for Finance and Economic Planning, determines that all issues of all denominations of the East African Currency Board notes and coins having ceased to be legal tender on 14th September, 1967, and 10th April, 1969, respectively, but continuing to be exchanged at par for Kenya currency notes and coins at all Offices of the Bank shall be withdrawn on 31st December, 1972, after which date the Bank shall demonetize and discontinue the exchange of the said notes and coins for Kenya currency notes and coins.

THE CENTRAL BANK OF KENYA- WITHDRAWAL OF EAST AFRICAN SHILLINGS, 1972

The Central Bank of Kenya, with the approval of the Cabinet Secretary for Finance and Economic Planning, determines that all issues of all denominations of the East African Currency Board notes and coins having ceased to be legal tender on 14th September, 1967, and 10th April, 1969, respectively, but continuing to be exchanged at par for Kenya currency notes and coins at all Offices of the Bank shall be withdrawn on 31st December, 1972, after which date the Bank shall demonetize and discontinue the exchange of the said notes and coins for Kenya currency notes and coins.

THE CENTRAL BANK OF KENYA- DETERMINATION OF PAR VALUE OF THE KENYAN SHILLING, 1973

Revoked by Legal Notice 35 of 1973 on 2nd March, 1973

IN EXERCISE of the powers conferred by section 20 of the Central Bank of Kenya Act, I, Jomo Kenyatta, President and Commander-in-Chief of the Armed Forces of the Republic of Kenya, hereby with effect from the 16th February, 1973, determine the Par Value of the Kenya Shilling in terms of gold as follow:—

301.57143 Kenya Shillings to equal one troy ounce of fine gold.

THE CENTRAL BANK OF KENYA- DETERMINATION OF PAR VALUE OF THE KENYAN SHILLING, 1973

Revoked by Legal Notice 35 of 1973 on 2nd March, 1973

THE CENTRAL BANK OF KENYA- DETERMINATION OF PAR VALUE OF THE KENYAN SHILLING, 1973

The par value of the Kenya shilling determined in terms of gold, with effect from the 16th February, 1973, is as follows—

301.586 Kenya shillings equal one troy ounce of fine gold.

Legal Notice No. 29 of 1973 is hereby cancelled.

DETERMINATION OF PAR VALUE OF THE KENYAN SHILLING, 1973

The par value of the Kenya shilling determined in terms of gold, with effect from the 16th February, 1973, is as follows—

301.586 Kenya shillings equal one troy ounce of fine gold.

Legal Notice No. 29 of 1973 is hereby cancelled.

CENTRAL BANK OF KENYA- DESCRIPTION OF NEW COIN, 1973

IN EXERCISE of the powers conferred by section 22 (2) of the Central Bank of Kenya Act, the Minister for Finance and Economic Planning, acting on the recommendation of the Central Bank of Kenya, has determined the denomination, inscriptions, form and material of a five-shilling coin to be issued by the Central Bank of Kenya as follows:—

| 1. |

The coin shall have the denomination of five shillings and shall bear the date 1973 as the year of issue.

|

| 2. |

The design of the new coin shall incorporate the following features—

| (a) |

the face of the coin shall bear a representation of the head of the President, His Excellency Mzee Jomo Kenyatta, C.G.H., M.P.;

|

| (b) |

the reverse of the coin shall incorporate the Kenya coat-of-arms, the words "Ten Years of Freedom", and the value in letters and figures.

|

|

| 3. |

Shape, composition and size—

Shape—9-sided, plain edges

Composition—Aluminium Bronze

Diameter—33 millimetres from centre of flat to opposite centre

Weight—13.9 grammes.

|

CENTRAL BANK OF KENYA- DESCRIPTION OF NEW COIN, 1973

The denomination, inscriptions, form and material of a five-shilling coin to be issued by the Central Bank of Kenya as follows:—

| 1. |

The coin shall have the denomination of five shillings and shall bear the date 1973 as the year of issue.

|

| 2. |

The design of the new coin shall incorporate the following features—

| (a) |

the face of the coin shall bear a representation of the head of the President, His Excellency Mzee Jomo Kenyatta, C.G.H., M.P.;

|

| (b) |

the reverse of the coin shall incorporate the Kenya coat-of-arms, the words "Ten Years of Freedom", and the value in letters and figures.

|

|

| 3. |

Shape, composition and size—

Shape—9-sided, plain edges

Composition—Aluminium Bronze

Diameter—33 millimetres from centre of flat to opposite centre

Weight—13.9 grammes.

|

THE CENTRAL BANK OF KENYA- DESCRIPTION OF NEW ISSUE OF BANK NOTES, 1974

IN EXERCISE of the powers conferred by section 22 (2) of the Central Bank of Kenya Act, the Minister for Finance and Economic Planning acting on the recommendation of the Central Bank of Kenya, hereby determines that the denominations, inscriptions, form, material and characteristics of new notes to be issued by the Central Bank of Kenya shall be as follows:—

| 1. |

The new notes shall have the denominations of five shillings, ten shillings, twenty shillings and one hundred shillings.

|

| 2. |

The designs or the new notes shall show features indigenous to Kenya and in addition to its individual characteristics, described below, each note shall incorporate—

| (a) |

on the front of the note—

| (i) |

a portrait of the President, His Excellency Mzee Jomo Kenyatta; |

| (ii) |

the title of the Bank in Kiswahili and English followed by the words "LEGAL TENDER FOR" and the denomination of the note in words in English and Kiswahili; |

| (iii) |

an ornamental motif in the centre, incorporating some features of Kenya's coat-of-arms and depicting the denomination of the note in words in English followed by the words "The First President of Kenya Mzee Jomo Kenyatta" followed by the words "FOR THE BOARD OF DIRECTORS", underneath which the signature of the Governor and a member of the Board of Directors of the Bank shall be inscribed. The paper of each note shall incorporate a lion's head, as the watermark, and a security thread. |

| (iv) |

a serial number in the vicinity of the top right hand and bottom left hand corner; |

| (v) |

the date of issue of the note in the vicinity of the bottom right hand corner; |

| (vi) |

the denomination of the note in English figures at each of the corners. |

|

| (b) |

on the back of the note, in addition to the individual characteristics pertaining to the back, the denomination of the note in words in English and—

| (i) |

in the cases of the one hundred shilling and the twenty shilling note the denomination of the note in English figures at three of the corners; |

| (ii) |

in the cases of the ten shilling and the five shilling note the denomination of the note in English figures at each of the corners. |

|

|

| 3. |

The individual characteristics of the various denominations of notes shall be as follows:—

|

| Sh. |

5

Size: 133.75 millimetres by 70 millimetres.

Basic colour: Brown.

Back: A coffee picker and coffee plantation with Mount Kenya in the background.

|

| Sh. |

10

Size: 140 millimetres by 73 millimetres.

Basic colour: Green.

Back: Dairy cattle in pasture with Mount Kenya in the background.

|

| Sh. |

20

Size: 146 millimetres by 76 millimetres.

Basic colour: Blue.

Back: Lions with Mount Kenya in the background.

|

| Sh. |

100

Size: 152 millimetres by 79 millimetres.

Basic colour: Purple.

Back: Statue of His Excellency the President and the Kenyatta Conference Centre with Mount Kenya in the background.

|

THE CENTRAL BANK OF KENYA- DESCRIPTION OF NEW ISSUE OF BANK NOTES, 1974

The denominations, inscriptions, form, material and characteristics of new notes to be issued by the Central Bank of Kenya shall be as follows:—

| 1. |

The new notes shall have the denominations of five shillings, ten shillings, twenty shillings and one hundred shillings.

|

| 2. |

The designs or the new notes shall show features indigenous to Kenya and in addition to its individual characteristics, described below, each note shall incorporate—

| (a) |

on the front of the note—

| (i) |

a portrait of the President, His Excellency Mzee Jomo Kenyatta; |

| (ii) |

the title of the Bank in Kiswahili and English followed by the words "LEGAL TENDER FOR" and the denomination of the note in words in English and Kiswahili; |

| (iii) |

an ornamental motif in the centre, incorporating some features of Kenya's coat-of-arms and depicting the denomination of the note in words in English followed by the words "The First President of Kenya Mzee Jomo Kenyatta" followed by the words "FOR THE BOARD OF DIRECTORS", underneath which the signature of the Governor and a member of the Board of Directors of the Bank shall be inscribed. The paper of each note shall incorporate a lion's head, as the watermark, and a security thread. |

| (iv) |

a serial number in the vicinity of the top right hand and bottom left hand corner; |

| (v) |

the date of issue of the note in the vicinity of the bottom right hand corner; |

| (vi) |

the denomination of the note in English figures at each of the corners. |

|

| (b) |

on the back of the note, in addition to the individual characteristics pertaining to the back, the denomination of the note in words in English and—

| (i) |

in the cases of the one hundred shilling and the twenty shilling note the denomination of the note in English figures at three of the corners; |

| (ii) |

in the cases of the ten shilling and the five shilling note the denomination of the note in English figures at each of the corners. |

|

|

| 3. |

The individual characteristics of the various denominations of notes shall be as follows:—

|

| Sh. |

5

Size: 133.75 millimetres by 70 millimetres.

Basic colour: Brown.

Back: A coffee picker and coffee plantation with Mount Kenya in the background.

|

| Sh. |

10

Size: 140 millimetres by 73 millimetres.

Basic colour: Green.

Back: Dairy cattle in pasture with Mount Kenya in the background.

|

| Sh. |

20

Size: 146 millimetres by 76 millimetres.

Basic colour: Blue.

Back: Lions with Mount Kenya in the background.

|

| Sh. |

100

Size: 152 millimetres by 79 millimetres.

Basic colour: Purple.

Back: Statue of His Excellency the President and the Kenyatta Conference Centre with Mount Kenya in the background.

|

THE CENTRAL BANK OF KENYA- WITHDRAWAL OF BANK NOTES, 1974

IN EXERCISE of the powers conferred by section 22 (3) of the Central Bank of Kenya Act, the Central Bank of Kenya hereby gives notice as follows:—

| 1. |

All notes of the Central Bank of Kenya of the denomination of one hundred shillings issued in pursuance of Legal Notices Nos. 252 of 1966, 47 of 1970 and 106 of 1970 are to be withdrawn.

|

| 2. |

All such notes shall cease to be legal tender on and after 13th January, 1975.

|

| 3. |

All such notes may be exchanged at their face value for legal tender during the period 13th December, 1974, to 12th January, 1975, at any of the places specified in the Schedule hereto, during normal working hours.

|

SCHEDULE (Paragraph 3)

| (i) |

The Central Bank of Kenya, Haile Selassie Avenue, Nairobi. |

| (ii) |

Any branch in Kenya of a licensed bank. |

| (iii) |

Any of the following offices of the Provincial Administration:— |

|

Province

|

Office

|

Place

|

|

(a) COAST

|

District Commissioner

|

Galole

|

|

District Commissioner

|

Kwale

|

|

District Commissioner

|

Lamu

|

|

District Officer

|

Taveta

|

|

(b) EASTERN

|

District Commissioner

|

Isiolo

|

|

District Commissioner

|

Lodwar

|

|

District Commissioner

|

Marsabit

|

|

(c) RIFT VALLEY

|

District Officer

|

Eldama Ravine

|

|

District Commissioner

|

Kabarnet

|

|

District Commissioner

|

Kajiado

|

|

District Commissioner

|

Kapenguria

|

|

District Commissioner

|

Maralal

|

|

District Commissioner

|

Narok

|

|

District Commissioner

|

Tambach

|

|

(d) NORTH-EASTERN

|

District Commissioner

|

Garissa

|

|

District Commissioner

|

Mandera

|

|

District Commissioner

|

Wajir

|

|

(e) WESTERN

|

District Commissioner

|

Busia

|

THE CENTRAL BANK OF KENYA- WITHDRAWAL OF BANK NOTES, 1974

| 1. |

All notes of the Central Bank of Kenya of the denomination of one hundred shillings issued in pursuance of Legal Notices Nos. 252 of 1966, 47 of 1970 and 106 of 1970 are to be withdrawn.

|

| 2. |

All such notes shall cease to be legal tender on and after 13th January, 1975.

|

| 3. |

All such notes may be exchanged at their face value for legal tender during the period 13th December, 1974 to 12th January, 1975, at any of the places specified in the Schedule hereto, during normal working hours.

|

SCHEDULE [para. 3]

| (i) |

The Central Bank of Kenya, Haile Selassie Avenue, Nairobi. |

| (ii) |

Any branch in Kenya of a licensed bank. |

| (iii) |

Any of the following offices of the Provincial Administration:— |

|

Province

|

Office

|

Place

|

|

(a) COAST

|

District Commissioner

|

Galole

|

|

District Commissioner

|

Kwale

|

|

District Commissioner

|

Lamu

|

|

District Officer

|

Taveta

|

|

(b) EASTERN

|

District Commissioner

|

Isiolo

|

|

District Commissioner

|

Lodwar

|

|

District Commissioner

|

Marsabit

|

|

(c) RIFT VALLEY

|

District Officer

|

Eldama Ravine

|

|

District Commissioner

|

Kabarnet

|

|

District Commissioner

|

Kajiado

|

|

District Commissioner

|

Kapenguria

|

|

District Commissioner

|

Maralal

|

|

District Commissioner

|

Narok

|

|

District Commissioner

|

Tambach

|

|

(d) NORTH-EASTERN

|

District Commissioner

|

Garissa

|

|

District Commissioner

|

Mandera

|

|

District Commissioner

|

Wajir

|

|

(e) WESTERN

|

District Commissioner

|

Busia

|

SPECIFIED PUBLIC ENTITIES UNDER SECTION 2

The Industrial Development Bank Limited.

SPECIFIED PUBLIC ENTITIES UNDER SECTION 2

The Industrial Development Bank Limited.

The Deposit Protection Fund Board.

SPECIFIED PUBLIC ENTITIES UNDER SECTION 2

The Industrial Development Bank Limited.

The Deposit Protection Fund Board.

The United States Agency for International Development.

SPECIFIED PUBLIC ENTITIES UNDER SECTION 2

The Industrial Development Bank Limited.

The Deposit Protection Fund Board.

The United States Agency for International Development.

The African Development Bank.

SPECIFIED PUBLIC ENTITIES UNDER SECTION 2

The Industrial Development Bank Limited.

The Deposit Protection Fund Board.

The United States Agency for International Development.

The African Development Bank.

The International Finance Corporation.

THE CENTRAL BANK OF KENYA- DESCRIPTION OF BANK NOTES, 1979

IN EXERCISE of the powers conferred by section 22 (2) of the Central Bank of Kenya Act, the Vice-President and Minister for Finance, acting on the recommendation of the Central Bank of Kenya, notifies that the Central Bank of Kenya will issue bank notes of five, ten, twenty and one hundred shillings denominations as follows:—

| (i) |

the description in words "SHILLINGI KUMI" in Swahili on the front face will be replaced by the inscription "KUMI" in enlarged capitals; |

| (ii) |

the description of the denomination in words in English on the front face will be omitted; |

| (iii) |

the figures on the back face will be substituted with the inscription "KUMI" in each case; |

| (iv) |

the words in English on the back face will be omitted. |

| (i) |

the size will be enlarged to 82 x 158mm; |

| (ii) |

the description of the denomination in words in English on the front face will be omitted; |

| (iii) |

varying shades of dark-brown colouration will be introduced to the existing range of colours appearing on the front face of the note; |

| (iv) |

varying shades of brownish colouration will be introduced to the existing range of colours on the back face of the note; |

| (v) |

the bluish colouration on Mount Kenya on the back face will be more intense. |

The notes will circulate alongside existing currency notes.

THE CENTRAL BANK OF KENYA- DESCRIPTION OF BANK NOTES, 1979

The Central Bank of Kenya will issue bank notes of five, ten, twenty and one hundred shillings denominations as follows:—

| (i) |

the description in words "SHILLINGI KUMI" in Swahili on the front face will be replaced by the inscription "KUMI" in enlarged capitals; |

| (ii) |

the description of the denomination in words in English on the front face will be omitted; |

| (iii) |

the figures on the back face will be substituted with the inscription "KUMI" in each case; |

| (iv) |

the words in English on the back face will be omitted. |

| (i) |

the size will be enlarged to 82 x 158mm; |

| (ii) |

the description of the denomination in words in English on the front face will be omitted; |

| (iii) |

varying shades of dark-brown colouration will be introduced to the existing range of colours appearing on the front face of the note; |

| (iv) |

varying shades of brownish colouration will be introduced to the existing range of colours on the back face of the note; |

| (v) |

the bluish colouration on Mount Kenya on the back face will be more intense. |

The notes will circulate alongside existing currency notes.

THE CENTRAL BANK OF KENYA- DESCRIPTION OF NEW ISSUE OF COMMEMORATIVE GOLD AND SILVER COINS, 1979

IN EXERCISE of the powers conferred by section 22 (2) of the Central Bank of Kenya Act, the Vice President and Minister for Finance, acting on the recommendation of the Central Bank of Kenya, notifies that, to commemorate the installation of His Excellency the President Daniel Toroitich arap Mai, the Central Bank of Kenya will issue gold and silver coins of the following descriptions:—

|

Gold coin—

|

|

|

|

|

Size

|

|

—

|

38.61mm diameter;

|

|

Thickness

|

|

—

|

2.44mm;

|

|

Weight

|

|

—

|

40 grams;

|

|

Gold content

|

|

—

|

916.6 gold per 1000 parts;

|

|

Face value

|

|

—

|

Sh. 3000;

|

|

Shape

|

|

—

|

Round;

|

|

Edges

|

|

—

|

Milled;

|

|

Finish

|

|

—

|

Frosted portrait against unfrosted background;

|

|

Reverse side

|

|

—

|

Bears Kenya Coat of Arms with inscriptions: 14TH OCTOBER 1978; 3000 SHILLINGS;

|

|

Obverse side

|

|

—

|

A portrait with the inscription: DANIEL TOROITICH ARAP MOI: PRESIDENT OF REPUBLIC OF KENYA.

|

|

|

|

|

|

|

Silver coin-

|

|

|

|

|

Size

|

|

—

|

38.61mm diameter

|

|

Thickness

|

|

—

|

2.87mm;

|

|

Weight

|

|

—

|

28.28 grams;

|

|

Silver content

|

|

—

|

925 silver per 1000 parts;

|

|

Face value

|

|

—

|

Sh. 200;

|

|

Shape

|

|

—

|

Round;

|

|

Edges

|

|

—

|

Milled;

|

|

Finish

|

|

—

|

Frosted portrait against unfrosted background;

|

|

Reverse side

|

|

—

|

Bears Kenya Coat of Arms with inscriptions: 14TH OCTOBER 1978: 200 SHILLINGS;

|

|

Obverse side

|

|

—

|

A portrait with the inscription: DANIEL TOROITICH ARAP MOI: PRESIDENT OF REPUBLIC OF KENYA.

|

THE CENTRAL BANK OF KENYA- DESCRIPTION OF NEW ISSUE OF COMMEMORATIVE GOLD AND SILVER COINS, 1979

To commemorate the installation of His Excellency the President Daniel Toroitich arap Mai, the Central Bank of Kenya will issue gold and silver coins of the following descriptions:—

|

Gold coin—

|

|

|

|

|

Size

|

|

—

|

38.61mm diameter;

|

|

Thickness

|

|

—

|

2.44mm;

|

|

Weight

|

|

—

|

40 grams;

|

|

Gold content

|

|

—

|

916.6 gold per 1000 parts;

|

|

Face value

|

|

—

|

Sh. 3000;

|

|

Shape

|

|

—

|

Round;

|

|

Edges

|

|

—

|

Milled;

|

|

Finish

|

|

—

|

Frosted portrait against unfrosted background;

|

|

Reverse side

|

|

—

|

Bears Kenya Coat of Arms with inscriptions: 14TH OCTOBER 1978; 3000 SHILLINGS;

|

|

Obverse side

|

|

—

|

A portrait with the inscription: DANIEL TOROITICH ARAP MOI: PRESIDENT OF REPUBLIC OF KENYA.

|

|

|

|

|

|

|

Silver coin-

|

|

|

|

|

Size

|

|

—

|

38.61mm diameter

|

|

Thickness

|

|

—

|

2.87mm;

|

|

Weight

|

|

—

|

28.28 grams;

|

|

Silver content

|

|

—

|

925 silver per 1000 parts;

|

|

Face value

|

|

—

|

Sh. 200;

|

|

Shape

|

|

—

|

Round;

|

|

Edges

|

|

—

|

Milled;

|

|

Finish

|

|

—

|

Frosted portrait against unfrosted background;

|

|

Reverse side

|

|

—

|

Bears Kenya Coat of Arms with inscriptions: 14TH OCTOBER 1978: 200 SHILLINGS;

|

|

Obverse side

|

|

—

|

A portrait with the inscription: DANIEL TOROITICH ARAP MOI: PRESIDENT OF REPUBLIC OF KENYA.

|

THE CENTRAL BANK OF KENYA- DESCRIPTION OF NEW KENYA CURRENCY NOTES AND COINS, 1980

IN EXERCISE of the powers conferred by section 22 of the Central Bank of Kenya Act, the Vice-President and Minister for Finance, acting on the recommendation of the Central Bank of Kenya, notifies that the Central Bank of Kenya will issue new currency notes and coins bearing a portrait of the President and Commander-in-Chief of the Armed Forces, His Excellency Daniel Toroitich arap Moi, C.G.H., M.P., with the following descriptions:—

| 1. |

| (a) |

Shillings 100 Note:

Basic Colours: Front face—mauve and red in green background.

Back face—mauve.

Main back face characteristics: Kenyatta Conference Centre with Mount Kenya in the background.

Size: 158 mm x 82 mm.

|

| (b) |

Shillings 50 Note:

Basic Colours: Front face—red.

Back face—olive in violet background.

Main back face characteristics: Jomo Kenyatta International Airport.

Size: 152 mm x 79 mm.

|

| (c) |

Shillings 20 Note:

Basic Colours: Front face—blue.

Back face—blue.

Main back face characteristics: Ladies reading a newspaper in an adult literacy class.

Size: 146 mm x 76 mm.

|

| (d) |

Shillings 10 Note:

Basic Colours: Front face—green.

Back face—green.

Main back face characteristics: School milk scheme depicting a boy and a girl taking milk with cattle in the background.

Size: 140 mm x 73 mm.

|

| (e) |

Shillings 5 Note:

Basic Colours: Front face—light brown.

Back face—light brown.

Main back face characteristics: Buffaloes and giraffes.

Size: 133 mm x 70 mm.

|

The shs 100, shs 50, shs 20, shs 10 and shs 5 notes depict Kenya's coat of arms and the portrait of His Excellency Daniel Toroitich arap Moi. The notes also incorporate a lion's head as a watermark and a security thread.

|

| 2. |

| (a) |

sh 1: Composition cupro-nickel (75% copper and 25% nickel);

Weight — 7.78 grams

Diameter — 27.74 mm.

|

| (b) |

50 cent: Composition cupro-nickel (75% copper and 25% nickel);

Weight — 3.89 grams.

Diameter — 20.96 mm.

|

| (c) |

10 cent: Composition nickel brass (79% copper, 20% zinc and 1% nickel);

Weight — 9.45 grams

Diameter — 30.86 mm.

|

| (d) |

5 cent: Composition nickel brass (79% copper, 20% zinc and 1% nickel);

Weight — 5.67 grams

Diameter — 25.48 mm.

|

The obverse of all denominations of coins shows the head of the President with the inscription: PRESIDENT OF REPUBLIC OF KENYA DANIEL TOROITICH ARAP Moi, whilst the reverse incorporates the coat of arms with the inscription: REPUBLIC OF KENYA.

The new notes and coins will circulate alongside the present issues of Kenya currency notes and coins.

|

THE CENTRAL BANK OF KENYA- DESCRIPTION OF NEW KENYA CURRENCY NOTES AND COINS, 1980

The Central Bank of Kenya will issue new currency notes and coins bearing a portrait of the President and Commander-in-Chief of the Armed Forces, His Excellency Daniel Toroitich arap Moi, C.G.H., M.P., with the following descriptions:—

| 1. |

| (a) |

Shillings 100 Note:

Basic Colours: Front face—mauve and red in green background.

Back face—mauve.

Main back face characteristics: Kenyatta Conference Centre with Mount Kenya in the background.

Size: 158 mm x 82 mm.

|

| (b) |

Shillings 50 Note:

Basic Colours: Front face—red.

Back face—olive in violet background.

Main back face characteristics: Jomo Kenyatta International Airport.

Size: 152 mm x 79 mm.

|

| (c) |

Shillings 20 Note:

Basic Colours: Front face—blue.

Back face—blue.

Main back face characteristics: Ladies reading a newspaper in an adult literacy class.

Size: 146 mm x 76 mm.

|

| (d) |

Shillings 10 Note:

Basic Colours: Front face—green.

Back face—green.

Main back face characteristics: School milk scheme depicting a boy and a girl taking milk with cattle in the background.

Size: 140 mm x 73 mm.

|

| (e) |

Shillings 5 Note:

Basic Colours: Front face—light brown.

Back face—light brown.

Main back face characteristics: Buffaloes and giraffes.

Size: 133 mm x 70 mm.

|

The shs 100, shs 50, shs 20, shs 10 and shs 5 notes depict Kenya's coat of arms and the portrait of His Excellency Daniel Toroitich arap Moi. The notes also incorporate a lion's head as a watermark and a security thread.

|

| 2. |

| (a) |

sh 1: Composition cupro-nickel (75% copper and 25% nickel);

Weight — 7.78 grams

Diameter — 27.74 mm.

|

| (b) |

50 cent: Composition cupro-nickel (75% copper and 25% nickel);

Weight — 3.89 grams.

Diameter — 20.96 mm.

|

| (c) |

10 cent: Composition nickel brass (79% copper, 20% zinc and 1% nickel);

Weight — 9.45 grams

Diameter — 30.86 mm.

|

| (d) |

5 cent: Composition nickel brass (79% copper, 20% zinc and 1% nickel);

Weight — 5.67 grams

Diameter — 25.48 mm.

|

The obverse of all denominations of coins shows the head of the President with the inscription: PRESIDENT OF REPUBLIC OF KENYA DANIEL TOROITICH ARAP Moi, whilst the reverse incorporates the coat of arms with the inscription: REPUBLIC OF KENYA.

The new notes and coins will circulate alongside the present issues of Kenya currency notes and coins.

|

THE CENTRAL BANK OF KENYA SPECIFIED BANKS AND FINANCIAL INSTITUTIONS, 1983

Revoked by Legal Notice 143 of 2003 on 22nd August, 2003

IN EXERCISE of the powers conferred by section 2 of the Central Bank of Kenya Act, the Central Bank of Kenya specifies for the purpose of the Act the banks and financial institutions licensed under the Banking Act which are set out in the Schedules hereto.

[Legal Notices Nos. 158 and 159 of 1971 are revoked]

SCHEDULE I

BANKS

Algemene Bank Nederland N.V.

Bank of Baroda

Bank of Credit & Commerce International (Overseas) Limited

Bank of India

Bank of Oman

Banque De L indochine Et De Suez

Barclays Bank of Kenya Limited

Citibank N.A.

Commercial Bank of Africa Limited

Grindlays Bank International (Kenya) Limited

Habib Bank A.G. Zurich

Kenya Commercial Bank Limited

Middle East Bank Kenya Limited

National Bank of Kenya Limited

Pan African Bank Limited

The Co-operative Bank of Kenya Limited

The First National Bank of Chicago

The Standard Bank Limited

SCHEDULE II

FINANCIAL INSTITUTIONS

Akiba Loans & Finances Limited

Arab Africa Finance Limited

Bank of Credit & Commerce International Finance (Kenya) Limited

Business Finance Company Limited

Capital Finance Limited

Commercial Bank of Africa Finance Co. Limited

Continental Credit Finance Limited

Credit Finance Corporation Limited

Diamond Trust of Kenya Limited

East African Acceptances Limited

First Chicago (Kenya) Limited

Grindlays International Finance (Kenya) Limited

Habib Zurich Finance Kenya Limited

Home Savings & Mortgages Limited

Housing Finance Co. of Kenya Limited

Industrial Development Bank Limited

Investments & Mortgages Limited

Jimba Credit Corporation Limited

Kenya Commercial Finance Co. Limited

Kenya Finance Corporation Limited

Kenya National Capital Corporation Limited

Lima Finance Limited

Mercantile Finance Company Limited

Middle African Finance Co. Limited

Mombasa Savings and Finance Limited

Nairobi Finance Corporation Limited

National Industrial Credit East Africa Limited

Nationwide Finance Co. Limited

Pan African Credit & Finance Limited

Rural & Urban Credit Finance Limited

Savings & Loan Kenya Limited

Southern Credit Finance Company Limited

Thabiti Finance Company Limited

The Co-operative Bank of Kenya Finance Limited

Union Credit Limited.

THE CENTRAL BANK OF KENYA SPECIFIED BANKS AND FINANCIAL INSTITUTIONS, 1983

Revoked by Legal Notice 143 of 2003 on 22nd August, 2003

IN EXERCISE of the powers conferred by section 2 of the Central Bank of Kenya Act, the Central Bank of Kenya specifies for the purpose of the Act the banks and financial institutions licensed under the Banking Act which are set out in the Schedules hereto.

[Legal Notices Nos. 158 and 159 of 1971 are revoked]

SCHEDULE I

BANKS

Algemene Bank Nederland N.V.

Bank of Baroda

Bank of Credit & Commerce International (Overseas) Limited

Bank of India

Bank of Oman

Banque Indosuez

Barclays Bank of Kenya Limited

Citibank N.A.

Commercial Bank of Africa Limited

Continental Bank of Kenya Limited

Grindlays Bank International (Kenya) Limited

Habib Bank A.G. Zurich

Kenya Commercial Bank Limited

Middle East Bank Kenya Limited

National Bank of Kenya Limited

Pan African Bank Limited

The Co-operative Bank of Kenya Limited

The First National Bank of Chicago

The Standard Bank PLC

SCHEDULE II

FINANCIAL INSTITUTIONS

Akiba Loans & Finances Limited

Arab Africa Finance Limited

Bank of Credit & Commerce International Finance (Kenya) Limited

Business Finance Company Limited

Capital Finance Limited

Commercial Bank of Africa Finance Co. Limited

Continental Credit Finance Limited

Credit Finance Corporation Limited

Diamond Trust of Kenya Limited

East African Acceptances Limited

First Chicago (Kenya) Limited

Grindlays International Finance (Kenya) Limited

Habib Zurich Finance Kenya Limited

Home Savings & Mortgages Limited

Housing Finance Co. of Kenya Limited

Industrial Development Bank Limited

Investments & Mortgages Limited

Jimba Credit Corporation Limited

Kenya Commercial Finance Co. Limited

Kenya Finance Corporation Limited

Kenya National Capital Corporation Limited

Lima Finance Limited

Mercantile Finance Company Limited

Middle African Finance Co. Limited

Mombasa Savings and Finance Limited

Nairobi Finance Corporation Limited

National Industrial Credit East Africa Limited

Nationwide Finance Co. Limited

Pan African Credit & Finance Limited

Rural & Urban Credit Finance Limited

Savings & Loan Kenya Limited

Southern Credit Finance Limited

Thabiti Finance Company Limited

The Co-operative Bank of Kenya Finance Limited

Union Credit Limited.

THE CENTRAL BANK OF KENYA SPECIFIED BANKS AND FINANCIAL INSTITUTIONS, 1983

Revoked by Legal Notice 143 of 2003 on 22nd August, 2003

THE CENTRAL BANK OF KENYA- DESCRIPTION OF NEW ISSUE OF SHILLINGS COIN, 1985

IN EXERCISE of the powers conferred by section 22 (2) of the Central Bank of Kenya Act, the Minister for Finance, acting on the recommendations of the Central Bank of Kenya, determines and notifies that the denomination, inscriptions, form, material and characteristics of a new five shillings coin to be issued by the Central Bank of Kenya shall be as follows—

| 1. |

Denomination: The denomination of the new coin shall be five shillings;

|

| 2. |

Design Features: The coin shall incorporate the following inscriptions—

| (i) |

On the obverse side: the portrait of His Excellency, President Daniel Toroitich arap Moi and the inscription: PRESIDENT OF REPUBLIC OF KENYA, DANIEL TOROITICH ARAP MOI; |

| (ii) |

On the reverse side: the Kenya Coat of Arms and the inscriptions: REPUBLIC OF KENYA: 1985: 5; FIVE SHILLINGS; |

|

| 3. |

Metal Content: The metal alloy shall be cupronickel made up of 75% copper and 25% nickel;

|

| 4. |

Other Features:

Shape: 7 lobed

Weight: 13.5 grammes

Diameter: 30 millimeters

Edge: Plain

The new coin shall be legal tender in Kenya with effect from the 15th October, 1985 and nothing in this notice shall be construed as withdrawing the five shillings note as specified under L.N. No. 258 of 1979 which shall continue to be legal tender in Kenya.

|

THE CENTRAL BANK OF KENYA- DESCRIPTION OF NEW ISSUE OF SHILLINGS COIN, 1985

The denomination, inscriptions, form, material and characteristics of a new five shillings coin to be issued by the Central Bank of Kenya shall be as follows—

| 1. |

Denomination: The denomination of the new coin shall be five shillings;

|

| 2. |

Design Features: The coin shall incorporate the following inscriptions—

| (i) |

On the obverse side: the portrait of His Excellency, President Daniel Toroitich arap Moi and the inscription: PRESIDENT OF REPUBLIC OF KENYA, DANIEL TOROITICH ARAP MOI; |

| (ii) |

On the reverse side: the Kenya Coat of Arms and the inscriptions: REPUBLIC OF KENYA: 1985: 5; FIVE SHILLINGS; |

|

| 3. |

Metal Content: The metal alloy shall be cupronickel made up of 75% copper and 25% nickel;

|

| 4. |

Other Features:

Shape: 7 lobed

Weight: 13.5 grammes

Diameter: 30 millimeters

Edge: Plain

The new coin shall be legal tender in Kenya with effect from the 15th October, 1985 and nothing in this notice shall be construed as withdrawing the five shillings note as specified under L.N. No. 258 of 1979 which shall continue to be legal tender in Kenya.

|

THE CENTRAL BANK OF KENYA- DESCRIPTION OF NEW ISSUE OF TWO HUNDRED SHILLINGS NOTE, 1986

IN EXERCISE of the powers conferred by section 22 (2) of the Central Bank of Kenya Act, the Minister for Finance, acting on the recommendation of the Central Bank of Kenya, determines and notifies that the denomination, inscription, form, material and characteristics of a new two hundred shillings note to be issued by the Central Bank of Kenya shall be as follows:—

| 1. |

DENOMINATION:

The denomination of the new note shall be shillings 200 inscribed both in numerals and in words.

|

| 2. |

| (i) |

Front: The main colour shall be dark brown with blue, green and pink in the background. |

| (ii) |

Back: The main colour shall be dark brown with blue, green, orange and pink in the background. |

|

| 4. |

| (i) |

Front: The main features shall be the portrait of His Excellency, Daniel Toroitich arap Moi, C.G.H., M.P., President and Commander-in-Chief of the Armed Forces; the Kenya Coat of Arms; coffee cherries and tea. |

| (ii) |

Back: The main features shall be the Nyayo Fountain, wheat and maize. |

| (iii) |

Other Features: The note incorporates a clearly defined three dimensional water-mark of a lion's head as well as a continuous security thread. |

The new note will circulate alongside the present issue of Kenya currency notes and coins and shall be legal tender with effect from the 14th October, 1986.

|

THE CENTRAL BANK OF KENYA- DESCRIPTION OF NEW ISSUE OF TWO HUNDRED SHILLINGS NOTE, 1986

The denomination, inscription, form, material and characteristics of a new two hundred shillings note to be issued by the Central Bank of Kenya shall be as follows:—

| 1. |

DENOMINATION:

The denomination of the new note shall be shillings 200 inscribed both in numerals and in words.

|

| 2. |

| (i) |

Front: The main colour shall be dark brown with blue, green and pink in the background. |

| (ii) |

Back: The main colour shall be dark brown with blue, green, orange and pink in the background. |

|

| 4. |

| (i) |

Front: The main features shall be the portrait of His Excellency, Daniel Toroitich arap Moi, C.G.H., M.P., President and Commander-in-Chief of the Armed Forces; the Kenya Coat of Arms; coffee cherries and tea. |

| (ii) |

Back: The main features shall be the Nyayo Fountain, wheat and maize. |

| (iii) |

Other Features: The note incorporates a clearly defined three dimensional water-mark of a lion's head as well as a continuous security thread. |

The new note will circulate alongside the present issue of Kenya currency notes and coins and shall be legal tender with effect from the 14th October, 1986.

|

THE CENTRAL BANK OF KENYA- DESCRIPTION OF THE CENTRAL BANK OF KENYA'S 20TH ANNIVERSARY COMMEMORATIVE COINS, 1986

IN EXERCISE of the powers conferred by section 22 (2) of the Central Bank of Kenya Act, the Minister for Finance, acting on the recommendation of the Central Bank of Kenya, notifies that, to commemorate the 20th anniversary of the establishment of the Central Bank of Kenya, the Central Bank of Kenya will on 9th December, 1986 issue cupro-nickel coins of the following description:—

Face value: Sh. 500;

Metal content: Cupro-nickel (75 per cent copper, 25 per cent nickel);

Size: 38.61mm. in diameter;

Weight: 28.28 grams;

Shape: Round:

Edges: Milled;

Finish: Frosted portrait against unfrosted background;

| Oberse |

Side:

Bears the portrait of His Excellency the President with the inscriptions: DANIEL TOROITICH ARAP MOI, PRESIDENT OF REPUBLIC OF KENYA.

|

| Reverse |

side:

Bean Kenya Coat of Arms with the inscriptions: CENTRAL BANK OF KENYA, 14TH SEPTEMBER 1966-1986, FIVE HUNDRED SHILLINGS, 500.

|

THE CENTRAL BANK OF KENYA- DESCRIPTION OF THE CENTRAL BANK OF KENYA'S 20TH ANNIVERSARY COMMEMORATIVE COINS, 1986

To commemorate the 20th anniversary of the establishment of the Central Bank of Kenya, the Central Bank of Kenya will on 9th December, 1986 issue cupro-nickel coins of the following description:—

Face value: Sh. 500;

Metal content: Cupro-nickel (75 per cent copper, 25 per cent nickel);

Size: 38.61mm. in diameter;

Weight: 28.28 grams;

Shape: Round:

Edges: Milled;

Finish: Frosted portrait against unfrosted background;

| Oberse |

Side:

Bears the portrait of His Excellency the President with the inscriptions: DANIEL TOROITICH ARAP MOI, PRESIDENT OF REPUBLIC OF KENYA.

|

| Reverse |

side:

Bean Kenya Coat of Arms with the inscriptions: CENTRAL BANK OF KENYA, 14TH SEPTEMBER 1966-1986, FIVE HUNDRED SHILLINGS, 500.

|

THE CENTRAL BANK OF KENYA- DESCRIPTION OF TEN AND ONE HUNDRED SHILLINGS NOTE, 1989

IN EXERCISE of the powers conferred by section 22 (2) of the Central Bank of Kenya Act, the Vice-President and Minister for Finance, acting on the recommendation of the Central Bank of Kenya, determines and notifies that the denominations, inscriptions, form, material and characteristics of new designs of ten and one hundred shillings notes to be issued by the Central Bank of Kenya shall be as follows:

| (1) |

| (a) |

Denomination: The denomination of the note shall be shillings 10 inscribed both in numericals and in words; the former to be inscribed at the four corners of bath the front and back of the note.

|

| (b) |

| (i) |

Front: The main colour is green with blue and brown in the background. |

| (ii) |

Back: The main colour is green with blue, brown and purple, in the background. |

|

| (d) |

| (i) |

Front: The main features shall be the portrait of His Excellency Daniel Toroitich arap Moi, C.G.H., M.P., President and Commander-in-Chief of the Armed Forces of the Republic of Kenya; the Kenya Coat of Arms; and a rose flower. The title of the Bank in both Kiswahili and English shall be at the top left-hand side; one set of numbers shall be in a vertical line next to the watermark, and the other set shall be horizontal to the right of the portrait. The Kiswahili inscription shall be at the bottom. |

| (ii) |

Back: The main features shall be an. institution of higher learning with two pairs of students, one pair in academic gowns; a diploma certificate on the left hand edge of the note; a key on the right edge of the note and Mt. Kenya in the background. The English inscription shall be at the top. |

| (iii) |

Other features: The note incorporates a clearly defined three dimensional watermark of a lion's head as well as a continuous security thread. |

|

|

| (2) |

One Hundred Shillings note:

| (a) |

Denomination: The denomination of the note shall be shillings 100 inscribed both in numericals and in words; the former to be inscribed at the if our corners of both the face and the back of the note.

|

| (b) |

| (i) |

Front: The main colour as purple with red and green in the background. |

| (ii) |

Back: The main colour is purple with red and brown in the background. |

|

| (d) |

| (i) |

Front: The main features shall be the portrait of His Excellency Daniel Toroitich arap Moi, C.G.H., M.P., President and Commander-in-Chief of the Armed Forces of the Republic of Kenya; the Kenya Coat of Arms; and a rose flower. The title of the Bank in both Kiswahili and English shall be at the top left; one set of numbers shall be in a vertical line next to the watermark, and other set shall be horizontal to the right of the portrait. The Kiswahili inscription shall be at the bottom. |

| (ii) |

Back: The main features shall be the Nyayo Monument surrounded by National flags; the four engravings on the Nyayo Monument to the right edge of the note; 25 years of Uhuru Monument to the bottom left edge of the note; and Mt. Kenya in the background. |

| (iii) |

Other features: The note incorporates a clearly defined three dimensional watermark of a lion's head as well as continuous security thread. |

|

The new notes will circulate alongside the present issues of Kenya currency notes and coins with effect from the 17th October, 1989.

|

IN EXERCISE of the powers conferred by section 14 (1) of the Central Bank of Kenya Act, I, Daniel Toroitich arap Moi, President and Commander-in-Chief of the Armed Forces of the Republic of Kenya, being satisfied that such a waiver is in the interest and likely to promote the objects of the Central Bank of Kenya, waive the provision of section 14 (1) of the Act to the extent necessary to enable—

JOSEPH TENDENEI ARAP LETING'

to hold the appointment of the director of the Central Bank of Kenya.

THE CENTRAL BANK OF KENYA- INCREASE IN CAPITAL, 1989

IN EXERCISE of the powers conferred by section 8 (3) of the Central Bank of Kenya Act, the Vice-President and Minister for Finance directs that the paid-up capital of the Central Bank of Kenya shall be increased by transfer from its General Reserve Fund to its capital account of four hundred and seventy-four million shillings.

THE CENTRAL BANK OF KENYA- DESCRIPTION OF TEN AND ONE HUNDRED SHILLINGS NOTE, 1989

The denominations, inscriptions, form, material and characteristics of new designs of ten and one hundred shillings notes to be issued by the Central Bank of Kenya shall be as follows:

| (1) |

| (a) |

Denomination: The denomination of the note shall be shillings 10 inscribed both in numericals and in words; the former to be inscribed at the four corners of bath the front and back of the note.

|

| (b) |

| (i) |

Front: The main colour is green with blue and brown in the background. |

| (ii) |

Back: The main colour is green with blue, brown and purple, in the background. |

|

| (d) |

| (i) |

Front: The main features shall be the portrait of His Excellency Daniel Toroitich arap Moi, C.G.H., M.P., President and Commander-in-Chief of the Armed Forces of the Republic of Kenya; the Kenya Coat of Arms; and a rose flower. The title of the Bank in both Kiswahili and English shall be at the top left-hand side; one set of numbers shall be in a vertical line next to the watermark, and the other set shall be horizontal to the right of the portrait. The Kiswahili inscription shall be at the bottom. |

| (ii) |

Back: The main features shall be an. institution of higher learning with two pairs of students, one pair in academic gowns; a diploma certificate on the left hand edge of the note; a key on the right edge of the note and Mt. Kenya in the background. The English inscription shall be at the top. |

| (iii) |

Other features: The note incorporates a clearly defined three dimensional watermark of a lion's head as well as a continuous security thread. |

|

|

| (2) |

One Hundred Shillings note:

| (a) |

Denomination: The denomination of the note shall be shillings 100 inscribed both in numericals and in words; the former to be inscribed at the if our corners of both the face and the back of the note.

|

| (b) |

| (i) |

Front: The main colour as purple with red and green in the background. |

| (ii) |

Back: The main colour is purple with red and brown in the background. |

|

| (d) |

| (i) |

Front: The main features shall be the portrait of His Excellency Daniel Toroitich arap Moi, C.G.H., M.P., President and Commander-in-Chief of the Armed Forces of the Republic of Kenya; the Kenya Coat of Arms; and a rose flower. The title of the Bank in both Kiswahili and English shall be at the top left; one set of numbers shall be in a vertical line next to the watermark, and other set shall be horizontal to the right of the portrait. The Kiswahili inscription shall be at the bottom. |

| (ii) |

Back: The main features shall be the Nyayo Monument surrounded by National flags; the four engravings on the Nyayo Monument to the right edge of the note; 25 years of Uhuru Monument to the bottom left edge of the note; and Mt. Kenya in the background. |

| (iii) |

Other features: The note incorporates a clearly defined three dimensional watermark of a lion's head as well as continuous security thread. |

|

The new notes will circulate alongside the present issues of Kenya currency notes and coins with effect from the 17th October, 1989.

|

REGULATION OF INTEREST RATES AND TERMS OF CREDIT OF SPECIFIED BANKS AND SPECIFIED FINANCIAL INSTITUTIONS

| (a) |

The minimum rate of interest payable by specified banks and specified financial institutions on deposits or savings shall be 13.5 per cent per annum.

|

| (b) |

The maximum rate of interest which specified banks may charge for loans or advances granted for a term not exceeding three (3) years shall be 16.5 per cent per annum calculated on a reducing balance method, with monthly rests.

|

| (c) |

The maximum rate of interest which specified banks may charge for loans or advances granted for a term exceeding three(3) years shall be 19 per cent per annum calculated on a reducing balance method, with monthly rests:

Provided that interest rates on term loans granted for a period exceeding three (3) years outstanding in the books of specified banks on 31st March, 1990, shall continue at existing rates until 31st March, 1991, when interest rates may be re-negotiated between the parties subject to the maximum interest rate of 19 per cent per annum.

|

| (d) |

maximum rate of interest which specified financial institutions may charge for loans, advances or instalment facilities shall be 19 per cent per annum calculated on a reducing balance method, with monthly rests.

This notice shall be deemed to have come into effect on 1st April, 1990, and supersedes Gazette Notice No. 4939 of 1989 and Gazette No. 1458 of 1990.

|

THE CENTRAL BANK OF KENYA- INCREASE IN CAPITAL, 1989

The paid-up capital of the Central Bank of Kenya shall be increased by transfer from its General Reserve Fund to its capital account of four hundred and seventy-four million shillings.

THE CENTRAL BANK OF KENYA- DESCRIPTION OF NEW ISSUE OF FIFTY SHILLINGS NOTE, 1990

IN EXERCISE of the powers conferred by section 22 (2) of the Central Bank of Kenya Act, the Vice-President and Minister for Finance, acting on the recommendation of the Central Bank of Kenya, determines and notifies that the denomination, inscriptions, form, material and characteristics of new design of fifty shillings note to be issued by the Central Bank of Kenya shall be as follows:

| 1. |

DENOMINATION:

The denomination of the note shall be shillings 50 inscribed both in numerals and in words; the former to be inscribed at the four corners of both the front and back of the note:

|

| 2. |

| (i) |

Front.— The main colour shall be red with dark blue and brown in the background. |

| (ii) |

Back.— The main colour shall be green with red in the background. |

|

| 4. |

| (i) |

Front.— The main features shall be the portrait of His Excellency Daniel Toroitich arap Moi, C.G.H., M.P., President and Commander-in-Chief of the Armed Forces of the Republic of Kenya; the Kenya Coat of Arms; a rose flower and the title of the Bank in large letters reading "BANK KUU YA KENYA" and in small letters "CENTRAL BANK OF KENYA". |

| (ii) |

Back.— The main features shall be Office of the President and Kenyatta International Conference Centre and Kenya Flag in the background. |

| (iii) |

Other Features.— The note bears a distinct water-mark depicting a lion's head as well as a continuous security thread. |

The new note will circulate alongside the present issues of Kenya Currency notes.

|

REGULATION OF INTEREST RATES AND TERMS OF CREDIT OF SPECIFIED BANKS AND SPECIFIED FINANCIAL INSTITUTIONS

| (a) |

The minimum rate of interest payable by specified banks and specified financial institutions on deposits or savings shall be 13.5 per cent per annum.

|

| (b) |

The maximum rate of interest which specified banks may charge for loans or advances granted for a term not exceeding three (3) years shall be 16.5 per cent per annum calculated on a reducing balance method, with monthly rests.

|

| (c) |

The maximum rate of interest which specified banks may charge for loans or advances granted for a term exceeding three(3) years shall be 19 per cent per annum calculated on a reducing balance method, with monthly rests:

Provided that interest rates on term loans granted for a period exceeding three (3) years outstanding in the books of specified banks on 31st March, 1990, shall continue at existing rates until 31st March, 1991, when interest rates may be re-negotiated between the parties subject to the maximum interest rate of 19 per cent per annum.

|

| (d) |

maximum rate of interest which specified financial institutions may charge for loans, advances or instalment facilities shall be 19 per cent per annum calculated on a reducing balance method, with monthly rests.

This notice shall be deemed to have come into effect on 1st April, 1990, and supersedes Gazette Notice No. 4939 of 1989 and Gazette No. 1458 of 1990.

|

THE CENTRAL BANK OF KENYA- DESCRIPTION OF THE CENTRAL BANK OF KENYA'S SILVER JUBILEE COMMEMORATIVE COINS, 1991

IN EXERCISE of the powers conferred by section 22 (2) of the Central Bank of Kenya Act, the Vice-President and Minister for Finance, acting on the recommendation of the Central Bank of Kenya, notifies that, to commemorate the 25th anniversary of the establishment of the Central Bank of Kenya, the Central Bank of Kenya will issue a commemorative coin of the following description:—

Face value: Sh. 1000;

Metal content: 925 silver;

Size: 38.61 mm. in diameter;

weight: 28.28 grams;

Shape: Round;

Edges: Milled;

Finish: Frosted proof;

| Obverse |

Side:

Bears the portrait of His Excellency the President with inscriptions: DANIEL TOROITICH ARAP MOI, PRESIDENT OF REPUBLIC OF KENYA.

|

| Reverse |

Side:

Bears Kenya Coat of Altos with the inscriptions: CENTRAL BANK OF KENYA, SILVER JUBILEE 1991, ONE THOUSAND SHYLLINGS, 1000.

|

THE CENTRAL BANK OF KENYA- DESCRIPTION OF NEW ISSUE OF FIFTY SHILLINGS NOTE, 1990

The denomination, inscriptions, form, material and characteristics of new design of fifty shillings note to be issued by the Central Bank of Kenya shall be as follows:

| 1. |

DENOMINATION:

The denomination of the note shall be shillings 50 inscribed both in numerals and in words; the former to be inscribed at the four corners of both the front and back of the note:

|

| 2. |